So how does the whole process of sending and receiving of e-Invoice is like and how long does it take for the validation process?

While it involves a series of complex procedures to ensure a safe digital transaction between supplier and buyer, most of the processes will be conducted within the system, and does not require user’s intervention, and for the validation process, according to LHDN, it will be conducted electronically, which can be done instantly or near-instantly.

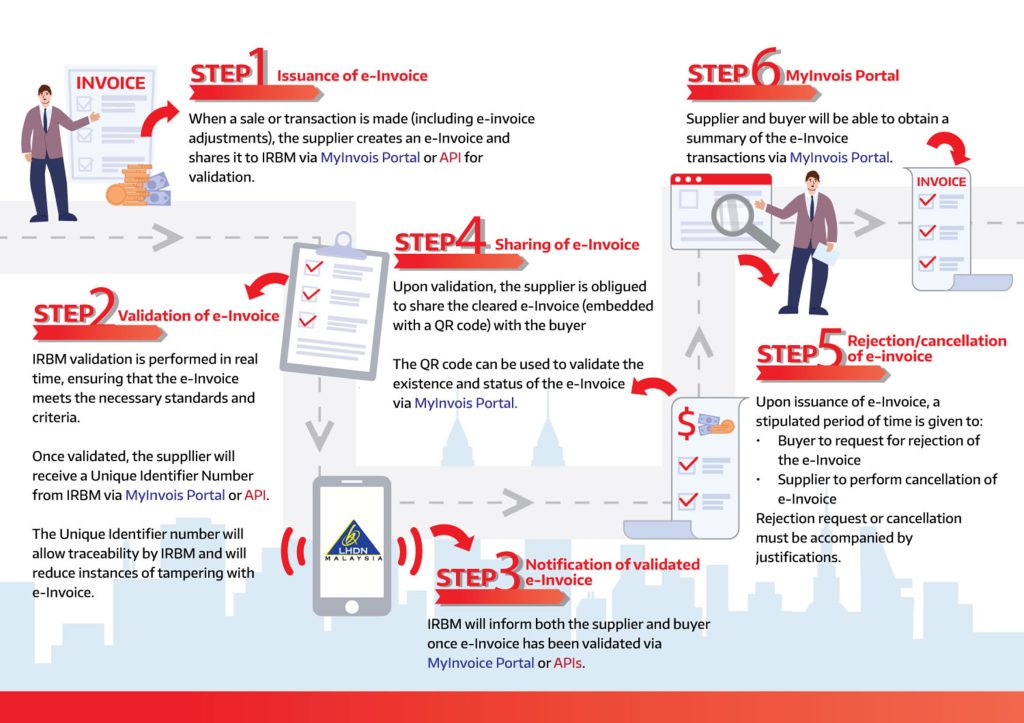

Step 1: Issuance of e-Invoice. The whole e-invoice process begins when a sale and or transaction is made (including e-invoice adjustments), which the supplier or sender create and e-Invoice to share to IRBM via Myinvoice Portal or API for validation. For accounting solution such as AutoCount, this feature is connected through API, by including e-Invoice within our system, users can have a more complete and automated invoicing process, without the need of accessing portal often to send and receive invoices.

Step 2: Validation of e-Invoice. As the submitted data needs to be validate before release, to ensure the e-Invoice meets the necessary standards and criteria, and according to info provided by LHDN, the validation process by IRBM is in real time or near-instantly.

After the validation process, the supplier will receive a Unique Identifier Number from IRBM within the platform they operates on, and the number will allow IRBM to trace as to reduce instances of tampering with e-Invoice, further strengthen the transaction’s safety and transparency.

Step 3: Notification of validated e-Invoice. After e-Invoice validation, IRBM will notify both supplier and buyer, either in MyInvoice Portal or APIs.

Step 4: Sharing of e-Invoice. Upon validation, the supplier is obliqued to share the cleared e-Invoice with the buyer, with a QR code embedded within, which the purpose is to validate the existence of the e-invoice by enablling checking or view in official MyInvois portal.

Step 5: Rejection/Cancellation of e-Invoice. After the e-Invoice has been issued, a stipulated period of time is given, to allow buyer to request for rejection of the invoice or supplier to cancel the e-Invoice in the process. In this stage, any rejection or cancellation request must be accompanied by justifications.

Step 6: MyInvois Portal. While there might seems like there are a series of complex procedures involved to send and share invoices, but worry not, with solution such as AutoCount, the e-Invoice feature will be embedded within the system, which users only have to select or enter some basic detail to generate invoices, and let the system automates the rest while keeping you updated, integrating official e-Invoicing within the system also maintain a better data integrity, accuraccy and safety.

A revision to the new e-Invoice implementation timeline for businesses has been announced during the Malaysian Budget 2024, with an update of the postponement of the start date and a shorter target timeframe for full implementation for every taxpayer.

The updated detailed timeline is as follows:

1 August 2024: Implement on taxpayers with an annual turnover of RM100 million and above.

1 January 2025: Implementation towards taxpayers with an annual turnover of RM25 million to RM100 million.

1 July 2025: To achieve full and comprehensive implementation on other remaining taxpayers.

Accountants urged the Government to permit small- and medium-sized enterprises (SMEs) to defer income tax instalment payments up to December 2020 instead of a three-month period ending in June 2020.

The Malaysian Institute of Certified Public Accountants and Malaysian Rating Corporation Bhd said that several SMEs were facing bankruptcy as their cash flow and revenue ran out with overhead expenses accumulated with the movement control order. The Government could consider extending the deferment until December 2020 as the impact of supply chain disruptions would be felt even after the COVID-19 outbreak ends.

The Government permits all SMEs to postpone income tax instalment payments for a three-month period commencing 1 April 2020 under the Prihatin Rakyat Economic Stimulus Package. This measure is in addition to the tax instalment payment postponement provided to impacted businesses in the tourism sector for six months, also beginning from 1 April 2020.

The accountants said that it is essential for financial institutions, namely commercial banks and development financial institutions, to step forward at this critical moment in Malaysia’s economic history. It is necessary that they continue to introduce funds into the economy and support economic activities by lending to viable businesses.

Otherwise, Malaysia could end up with thousands of business failures which would have dire implications on the financial system, economy and labour market. The two organisations said that the surge in business failures could also trigger large-scale social problems.

Malaysia, in principal, has committed to implement and adhere to Base Erosion and Profit Shifting (BEPS) Action Plan. It has officially joined the OECD Inclusive Framework on BEPS as Associate Members. The framework emphasises on four minimum standards:

• Action 5 – Countering Harmful Tax Practices More Effectively, Taking into Account Transparency and Substance

• Action 6 – Preventing the Granting of Treaty Benefits in Inappropriate Circumstances

• Action 13 – Guidance on Transfer Pricing Documentation and Country-by-Country Reporting

• Action 14 – Making Dispute Resolution Mechanisms More Effective

In addition, the Forum on Harmful Tax Practices (FHTP) has identified certain Malaysian incentives for evaluation on the basis that it provide preferential regimes for mobile geographical services activities related to intellectual property and non-intellectual property. The incentives are as follows:

Intellectual property incentives

Non-intellectual property incentives

Principal Hub

Pioneer Status (High Technology)

Biotechnology Industry (BioNexus)

MSC Malaysia

Biotechnology Industry (BioNexus)

MSC Malaysia

Principal Hub

Pioneer Status (Contract R&D)

Treasury Management Centre

Economic Development Regions [Iskandar Malaysia (IM), East Coast Economic Region (ECER), Sabah Development Corridor (SDC)]

Approved Services Project

Green Technology Services

Labuan Leasing Services

Foreign Fund Management

Inward re-insurance and offshore insurance

Malaysian International Trading Company

The Ministry of Finance (MoF) has released timelines where the above mentioned tax incentives shall be amended to meet the FHTP criteria. The Ministry of Finance is working with the Inland Revenue Board and related ministries/agencies to review the incentives in order to meet the criteria set under the FHTP.

Kindly visit the MoF website for further information.

IRB goes after taxpayers who have not filed tax returns for more than three years, 20 July 2017

The Inland Revenue Board (IRB) has launched an operation to track down 3,445 taxpayers who did not file their tax returns for more than three YAs. According to the IRB Deputy Chief Executive Officer (Policy), they will be focusing on external and table audits on 1,687 companies and 1,758 individuals from 17 July to 21 July 2017.

Company director charged for wilful evasion, 03 July 2017

The director of Ayam Wira Food Processing Sdn Bhd pleaded guilty to charges of wilful evasion under s 114(1)(b) of the Income Tax Act 1967 for making a false statement or entry in the corporate tax returns for YAs 2012 and 2013.

Based on the Inland Revenue Board (IRB)’s investigation, the company was found to have falsified purchase invoices from seven suppliers amounting to RM2,648,098 and RM374,448 for YAs 2012 and 2013 respectively. This led to an under-declaration of taxes amounting to RM662,024.50 and RM93,612.00 for YAs 2012 and 2013 respectively.

The court imposed a total fine of RM13,500 and penalty thrice the amount totalling RM2,266,909.50.

Director charged for sales tax evasion, 09 June 2017

A logistics company director was charged for submitting false sales tax declaration on contact lenses worth RM2.88m two years ago. The director was charged for:

• submitting declarations amounting to RM29,494.03 when the actual tax should have been RM311,052.75, and

• falsely declaring 10,817 boxes of imported contact lenses when 129,818 were brought into the country.

While making tax payment through various tax payment options, taxpayers have to specify a few information such as Name of Taxpayer/Employer, Income tax number/Employer number, Identity number and Payment Code.

Payment code is referring to the type of tax that categorized by Inland Revenue Board (IRB) or Lembaga Hasil Dalam Negeri (LHDN) Malaysia. Details on Tax Payment Code are tabulated in the table below.

Item

Payment Code

Description

1

084

Tax Instalment Payment – Individual

2

086

Tax Instalment Payment – Company

3

088

Investigation (Composite) Instalment Payment

4

090

Real Property Gain Tax Payment (RPGT)

5

095

Income Tax Payment (excluding instalment scheme)

6

150

Penalty Payment For Section 103A / 103 [tax not paid]

7

151

Payment Section 108

8

152

Penalty Payment For Section 108

9

153

Penalty Payment For Composite

10

154

Penalty Payment For Section 107C(9) [CP204 estimation not paid / 107B(3)

11

155

Penalty Payment For Section 107C(10) [CP204 under estimation by > 30%] / 107B(4)